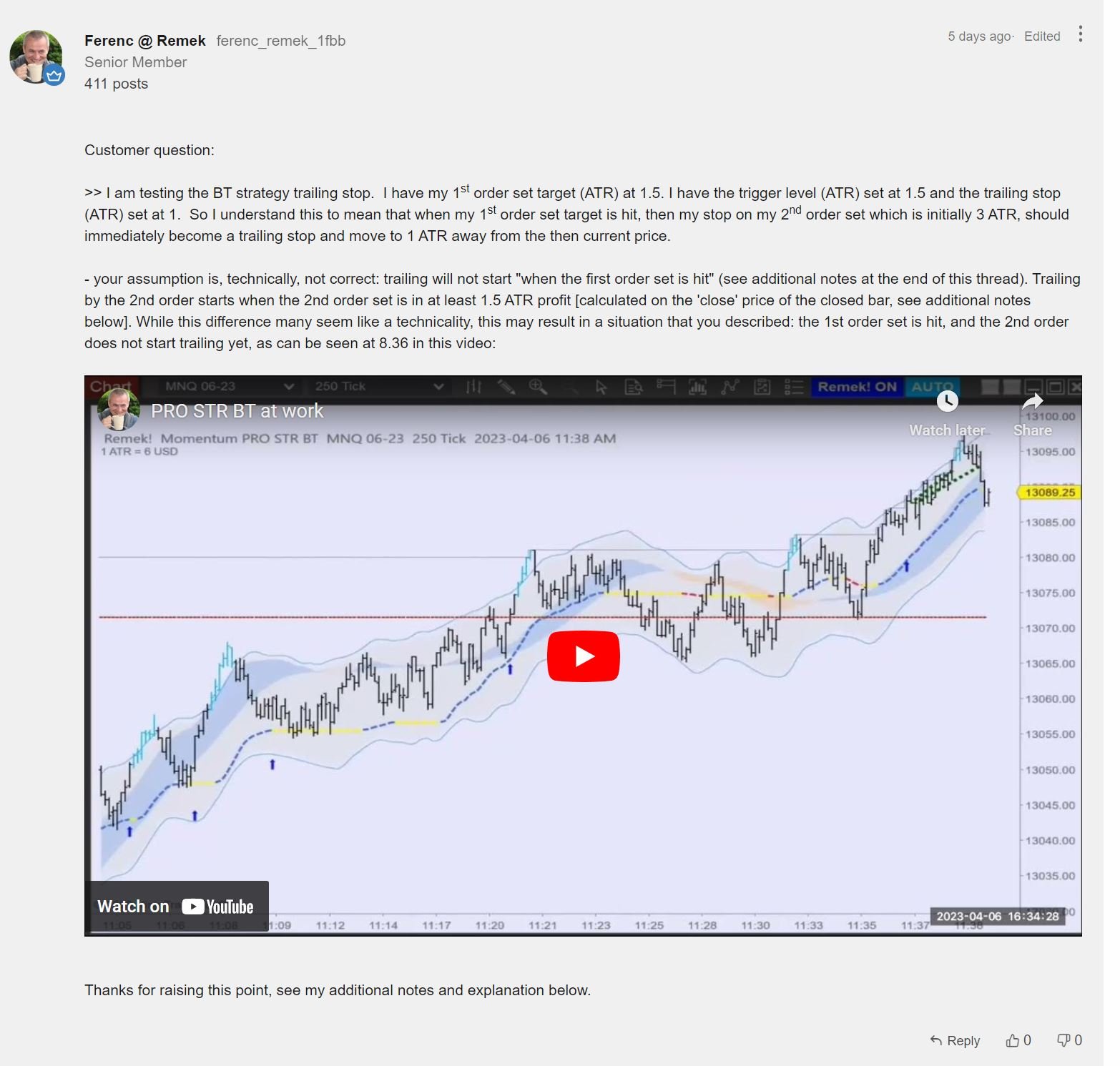

No market is ever in a hurry to give us a million dollars just like that. Trading is difficult, and many other traders, often with more skills, more technology and more pockets, are after the same edge we are. (We’re assuming you’re trading with an edge, for the purposes of this post.) Consequently, all edges are small. (Large edges would be like dollar bills on the sidewalk: they wouldn’t be there for long.)

To the point then: Remek! Momentum Standalones (PRO STR/BT/BTX) v3.5 is in the Remek! Lab!

Our software, professionally built on a rock-solid methodology, has been undergoing rigorous testing to ensure the product is faultless and ready for prime time. (We’re proud of the fact that we have not received from any of our thousands of active Remek! software customers one single bug report for several years now!)

The product is solid and should be ready for rollout soon. In the meantime, let me share with you some backtesting results in NT8 we ran with v3.5 (which will include a brand-new risk management engine!).

So a few pointers for those of you who are into backtesting (and please refer to our two backtesting videos on our youtube channel as well):

Backtesting is not proof. Of anything. If done well, it’s at its best, an indication, albeit an important one.

Backtesting is not the last step of an edge verification process, rather the first one, and there’s about 4-5 more steps after you have run some backtesting. (Also, the edge verification process is a circular process, as it includes regular monitoring whether our edge still exists.)

Backtesting is not real life. Your trades are not actually on the market, and will not move the market. Your real trades will.

Backtesting, run even with very good software, like NT8, has built-in limitations you must be aware of. Just a few for starters:

in backtesting when your price is hit, you get filled. In real life, often your order will not be filled. Over thousands of trades in backtesting, this can mean a big difference compared to real life trading.

in real life, there can be gap-ups, gap-downs, where your stop loss order may be skipped. Backtesting software cannot accurately recreate these scenarios.

in real life, there will be human errors, however automated you trade. Backtesting will not include those errors.

it’s easy to change a few settings here and there if you don’t like the results. But just be careful with never-ending “optimization”, so you don’t fit the question to the answer. Overly optimize settings look good on past data only and will collapse on future data. Your goal should be not chasing the best possible system, but to find a robust method that works on data that hasn’t happened yet.

to evaluate and understand backtesting results, we must know at least basic statistics and quantitative methods. Winning traders are friends with numbers.

and probably fifty other things we could think of (e.g. sample sizes, walk-forward etc.), so it’s easy to see, interpreting backtesting results is not so easy and the important clues are often hidden in the finer details.

Books on the art and science of backtesting can fill a library, and you should probably have a few good books on your trading shelf on backtesting methods.